* This is a compensated campaign in collaboration with Wells Fargo and Latina Bloggers Connect

At the end of each year, we all say we’re going to improve certain aspects of our life and money is one of the topics most notably referred to come the holidays and new year. In this economy, getting finances in order can be extremely difficult and can really beat us down in the new year. From maxing out credit cards on holiday gifts to work and income slowing down, money matters and getting financially fit can be very stressful. But my friends at Wells Fargo can help!

#WellsFargo is committed to making financial education and in-language resources available to Latino consumers. That includes providing customers with bilingual online tools, Spanish Text Banking, Spanish account statements, Spanish-language call centers, Spanish-speaking bankers in stores across the nation, and more.

As part of that commitment and in order to connect with the Hispanic community in a meaningful way, Wells Fargo recently collaborated with Telemundo for the “Conversemos de Tus Finanzas” campaign. The campaign is focused on empowering Hispanics to enhance their financial knowledge and help them to reach their financial goals. The campaign provides customized content, tools and resources around the important financial topics of money management and credit.

Check out these tips to getting your financial affairs in order this year so that each and every one to come will be a breeze!

Good habits you can implement now:

1.Cut out the crap: Ok, make a list of everything you spend money on in a month. Obviously you can’t cut out the electric bill or groceries but you can live without your daily Starbucks or that magazine you buy every month and neverread. be honest with yourself and make adjustments by making your lattes at home, reading that article online or cutting out those things that you’re throwing your money away on. A great exercise is to keep every receipt from every purchase you make for a week. You’d be surprised how quickly purchases add up and how little you have to show for it.

2. DIY: Find ways to do things yourself or at least do them cheaper. As mentioned above, make your own coffee or smoothies instead of spending $5 a day on your fix. Brown bag your lunch, watch your favorite shows online and can you your cable service. While it may seem like a pain at first, you’ll see how quickly you adjust to your new, affordable habits. The extra funds in your account will be enough to keep you on track!

3. Contribute holiday cash to an IRA: Did you receive some cash from gramma? Have a small chunk of savings just sitting around? Make it work for you by contributing to an IRA before you file your taxes.

4. Write-off resolution-related expenses: Join a weight loss program? Visiting a dietician or nutritionist? Keep your recepits this year, some of this stuff might qualify as a tax write-off, easily boosting your refund and putting more cash in your pocket with little effort.

5. Charity helps you and others: Charity is a great way to give back, either through volunteering your time or giving money or goods like used clothing. Don’t forget the monetary benefits of giving. Start 2012 right by keeping track of what you give for a refund booster on your tax return.

6. Save without lifting a finger: Reduce your taxable income next year by choosing to automatically contribute to your 401(k) next year, and set-up a free high-yield savings account online where you start by contributing even a small amount, say $25 per pay period, to an account you can’t easily drain.

7. Pay down debts: Too often we make lofty goals when it comes to paying down debt. Start with one credit card and focus in on one realistic first step, like doubling minimum payments toward one card with the highest interest, then slowly expand once you can meet this goal without skewing any of your other finances toward the negative.

8. Go Green: Yeah, conserving water and power, shopping locally and living greener also means saving green!

Credit Tips

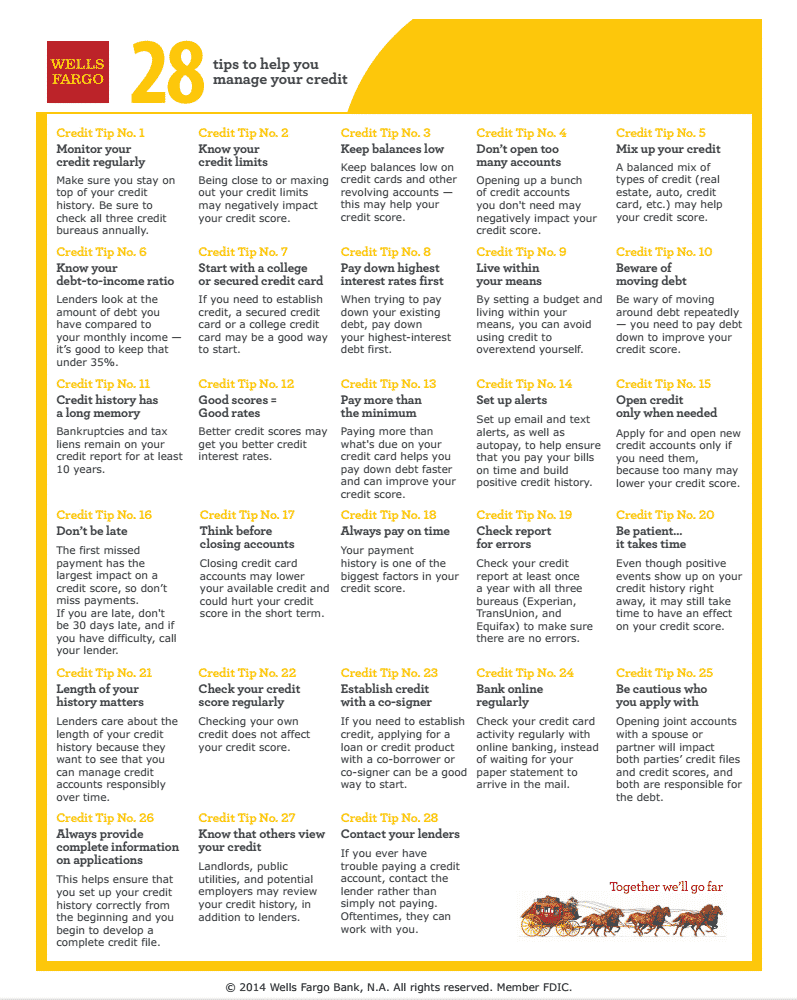

Establishing and constructing your credit is important in reaching your financial goals. Follow these tips to establish, improve and maintain your credit:

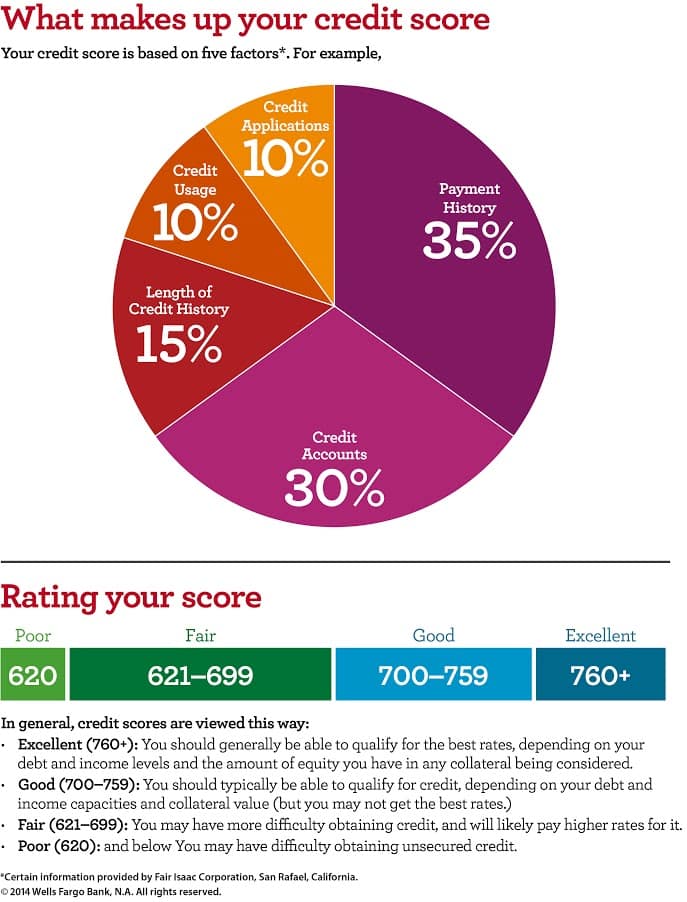

- Check your credit report annually

- Make sure your credit report contains current and accurate information. Errors could negatively impact your credit score and even be a sign of possible identity theft. Request a free copy of your credit report at least once a year from AnnualCreditReport.com or call toll-free 1-877-322-8228.

- Pay your bills on time

- Your payment history is one of the biggest factors in your credit score – including things that may surprise you like on-time payment of your rent and cell phone bill. Using free online tools, often available through your financial institution’s online banking, can help you develop a budget and create an automatic bill payment schedule.

- Set up alerts

- Set up email and text alerts, as well as autopay, to help ensure that you pay your bills on time and build positive credit history.

- Pay more than the minimum

- Paying more than what’s due on your credit card helps you pay down debt faster and can improve your credit score.

- Keep debt at no more than 35 percent of your gross monthly income

- Lenders look at the amount of debt a consumer has compared to their monthly income when making credit decisions.

- Contact your lenders

- If you ever have trouble paying a credit account, contact the lender rather than simply not paying. Oftentimes, they can work with you.

- Think before closing accounts

- Closing credit card accounts may lower your available credit and could hurt your credit score in the short term.

- Understand how strong credit impacts your bottom line. Your credit score influences the interest rate you qualify for. The lower the interest rate, the less you’ll pay in interest over time. Many sites, including Wells Fargo, offer calculators that help consumers understand how interest rates impact their payment and the total cost of the loan.

- Establish and maintain healthy credit – even if you don’t need a loan. Lenders aren’t the only people who use credit scores to make decisions – many insurance companies, cell phone providers and landlords do, too.

Money Management Tips

Money Management Tips

Money management is also very important when it comes to reaching your financial goals. Follow these tips so that managing your money is simple and effective:

- Learn where you can put your money

- Learn the types of accounts that are available and how to determine which ones you need. Here are some definitions to help you navigate your banking needs:

- Prepare a budget

- Checking account: A checking account offers easy access to your money for your daily transactional needs and helps keep your cash secure.

- Savings account: A savings account allows you to accumulate interest on funds you’ve saved for future needs.

- Certificate of Deposit (CD): Certificates of deposit, or CDs, allow you to invest your money at a set interest rate for a pre-set period of time.

- Money market account: Money market accounts are similar to savings accounts, but they require you to maintain a higher balance to avoid a monthly fee.

- Individual Retirement Accounts (IRAs): IRAs, or individual retirement accounts, allow you to save independently for your retirement.

- Before opening an account, it’s important to understand the terms and features.

- When you are thinking about opening an account, you should spend some time reviewing the features and requirements associated with the accounts you are considering.

- Learn how the FDIC safeguards your funds. The FDIC insures deposits and assesses the health of financial institutions across all 50 states.

- Understanding your income sources is one of the starting points towards creating a budget.

- Your annual gross income represents your total income before any taxes

- Tracking your expenses will help you spend your money more wisely. If you take the process step-by-step, it can be surprisingly easy to find out how you’re spending your money. Here’s how:

- Gather your financial statements.

- Create a list of monthly expenses.

- Examine your expenses or other deductions. “Take-home pay” represents your net income, specifically your income minus taxes, credits, and deductions.

- Fixed expenses

- Flexible expenses

- Discretionary expenses

- Saving for life’s special moments. Set your sights on specific goals to effectively target your savings strategy. Look for an online budgeting tool that helps you identify and track multiple goals at once.

Putting it all together in a budget. Create a budget in five easy steps.

- Step 1: Organize. At its core, a budget is a worksheet with two columns:

- Step 2: Track. For one month, keep a detailed log of all your spending

- Step 3: Analyze. At the end of the month, total your income and your

- Step 4: React. After looking at all of your expenses, separate them into one for income and one for expenses habits expenses and then subtract your expenses from your income categories and set a budget for each.

- Step 5: Review: Make a habit of reviewing your budget every month, particularly in the early stages.

- Manage cashflow and savings

- Track your spending. Online tools can make the process of tracking your

- Pay yourself first. If you’re having trouble finding ways to pay yourself first,

- Reduce your debt. If you find that you’re paying down your debt each month,

- Save for an emergency. Learn how much you should save in case of an

- Keep track of your account. An important step in managing your finances is

- Avoid overspending. Keeping an accurate record of your transactions is the spending completely automatic. If you choose to track your spending manually, get in the habit of consistently following a few basic practices:

- Save receipts

- Use your credit card

- Update your records

- Review the results try taking these steps to get into the habit:

- Figure out how much you can afford

- Set a personal payment goal

- Create a savings strategy but your balance doesn’t seem to budge, you may want to take a look at your payment strategy. Here are a few tips to help you make more headway:

- Organize your debt

- Prioritize your payments

- Consolidate your debt emergency consistently tracking your account activity best way to avoid spending more money than you have in your account.

Happy saving!

* This is a compensated campaign in collaboration with Wells Fargo and Latina Bloggers Connect

1 comment

Nice article